A short text that may upset adherents of inflation targeting, the devotion to which has acquired quasi-religious traits in Ukraine, should encourage them to seek alternatives.

The National Bank of Ukraine (NBU) has been implementing the inflation targeting regime since 2016. The inflation target has gradually reduced and since the end of 2019 has been 5% +/- 1 percentage point.

To demonstrate the success of this regime, the NBU traditionally points to decline in consumer inflation from 43.3% in 2015 to 4.1% in 2019 and 5% in 2020.

At the same time, the fact that the inflation surge in 2015 was driven by a sharp devaluation of the hryvnia, which took place, in fact, at the will of the National Bank itself, is out of the public eye.

In addition, other, no less important, aspects of the National Bank’s implementation of the inflation targeting regime remain “unnoticed”.

In particular, we are talking about the policy of “expensive money” (high interest rates), which resulted in decreased monetization of the economy, curtailment of lending activity and reorientation of banks to securities transactions – mainly government issued bonds.

The National Bank of Ukraine is also modestly silent about the fact that inflation rates in 2019 and 2020 were far from stable, as required by the Law of Ukraine On the National Bank of Ukraine: falling into the target range occurred on a rapid downward trend in 2019 and no less rapid, but already upward – in 2020.

Therefore, low inflation was short-lived: during the first quarter of 2021, the annual rate of consumer inflation accelerated from 5% to 8.5%.

Even the NBU interprets the correction to 8.4% in April as a temporary phenomenon and predicts “significant inflationary pressures to persist in the coming months”.

An increase in food and non-alcoholic beverages prices by 9.9% (the contribution was about 4 percentage points), due to the crop failure in 2020 and the rapid rise in world food prices had the biggest impact on the annual inflation rate (as of April).

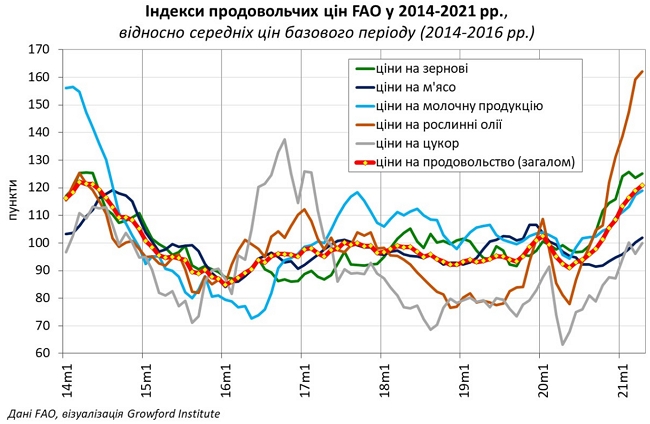

Over the last 12 months, the FAO Food Price Index has increased by 28.4 points or 30.8% to its highest value since May 2014.

The aggregate index went up as a result of the rise in price of vegetable oils over the current year by 99.5%, sugar – by 58.3%, grain – by 26.0%, dairy products – by 24.1%, meat – by 5, 1%.

The FAO Food Price Index in 2014-2021

relative average prices of basic period (2014-2016)

It is due to pressures of external conditions that domestic prices for sugar (65%) and oil (62.9%) had the highest annual growth rates.

The 90% rise in the price of eggs is driven largely by higher feed, due to the poor harvest and rising world grain prices.

The fact that the rapid growth of prices for these foods has not spread to the entire range of food products may be indirect evidence of the lack of excessive consumer demand.

In second place in terms of the impact on the overall inflation rate (with a contribution of about 2 percentage points) is the rise in price of housing and communal services by 26.5%.in April 2021 compared to April 2020

The main reason for higher prices for gas in annual terms by 89.9% was the rise in prices on the European market: Dutch hub TTF gas price has quadrupled over the past year – from 5.7 to 22.9 EUR / MWh.

The growth of electricity prices by 36.6% was purely administrative: the cancelation of the preferential rates for the population for the first 100 kWh from the beginning of the year and the establishment of a fixed price at the level of UAH 1.68 per kWh.

Fuel prices went up by 24.3% year on year due to rising world oil prices (over the past year, the Brent crude oil price rose from 25 to 67 USD/bbl).

That is, the acceleration of inflation in Ukraine was due to the shock of food supply (due to poor harvest), the impact of external conditions, as well as internal administrative factors.

However, these features of the current inflation surge did not prevent the National Bank of Ukraine from raising the key policy rate (from 6% to 7.5%) in order to overcome it.

The National Bank of Ukraine was prompted to take such a step by the logic of the inflation targeting regime, which means raising the rate to return inflation to the target by suppressing demand.

However, is such approach justified in a crisis?

Most central banks formally applying the inflation targeting, have shown by their actions over the past year that they are not justified.

Inflation is not an end in itself. Moreover, demand in a crisis should be stimulated, not suppressed.

Despite “tectonic shifts” in the practice of monetary regulation (including the central banks of developing countries), the Ukrainian central bank is trying to succeed in applying the three-decade-long recipes.

Meanwhile, at the other end of the world, events are taking place that could turn a page in monetary history called inflation targeting.

In April, US consumer inflation accelerated from 2.6% to 4.2% year on year to its highest level since the 2008 global financial crisis.

In terms of components, energy prices rose the most during the current year – by 25.1% (including gasoline – by 49.6%), while food prices went up by 2.4%, non-food goods and services (excluding energy) – by 3%.

That is, there is a possibility that the inflation surge in the United States is temporary.

However, occasional warnings are no less probable that we are witnessing the beginning of a new inflationary cycle (referring to the experience of the 1970s).

There are plenty of reasons for such assumptions. The amount of dollars issued from the beginning of 2020 to May 2021 almost doubled – the Fed’s balance sheet increased from USD 4.1 to 7.8 trillion.

In addition, there were numerous production disruptions (and hence supply disruptions) following quarantine restrictions and trade confrontation between the United States and China.

If these predictions come true, then the acceleration of inflation in the United States, given the exceptional position of the dollar in the global financial system, will provoke the corresponding processes on a global scale.

Under such conditions, inflation targeting (in the traditional sense) in small open economies loses its meaning.

Countries like Ukraine, even in the absence of domestic inflationary factors and maintaining exchange rate stability, will import inflation from abroad.

And if with increasing inflationary pressures the National Bank of Ukraine continues to be in the paradigm of the last century and tries to suppress inflation by squeezing domestic demand, such efforts will have minimal anti-inflationary effects, but will cause a marked decline in production (or slow economic recovery).

The past “secret to success” of inflation targeting in a number of developing countries was that it had taken place against a background of low inflation in the United States (the average annual rate over the past 30 years has been 2.3%) and other advanced economies.

But all good things must come to an end and the National Bank of Ukraine will obviously have to put up with the fact that the inflation targeting regime is not an eternal category, and the monetary regime and monetary policy should flexibly respond to changes in the external environment and domestic economic conditions.

What is more, the specialized law explicitly obliges the National Bank of Ukraine, in addition to inflation, to maintain financial stability and promote economic growth.

Head of the Money Markets Department at the Growford Institute Mykhailo Dzhus for Business.Censor.