On Bank Workers’ Day, May 20, the National Bank of Ukraine (NBU) published its own Strategy until 2025.

The strategy contains three “strategic pillars”:

• I. Promoting Economic Recovery and Growth;

• ІІ. Digital Finance as a Driver for Digitalization of the Economy;

• III. Institutional Development and Operational Excellence of the National Bank of Ukraine.

Each of the three pillars is detailed in four “strategic goals”, i.e. a total of 12 such goals, which is 5 more than in the previous version of the Strategy, which was in force in 2018-2020.

The main reason for the higher number of “strategic goals” was the excessive detailing of the third pillar of the Strategy for Domestic Development of the NBU itself.

It is as if someone in society should bother about “different pace of development” or “partial mismatched actions” of NBU units (from the list of “weaknesses” of the NBU).

All other “strategic goals” of the NBU in general correspond to their counterparts three years ago.

The fact that “promoting economic recovery” is highlighted in the Strategy may give the impression that the National Bank of Ukraine has finally reconsidered its “orthodox” position and followed the path of many central banks, which have significantly shifted the focus of their policy towards addressing the real sector of the economy.

However, this is only at first glance. Looking “inside” the first strategic pillar, we see that the NBU is going to help the economy recover by achieving the following goals:

1. maintaining macroeconomic stability;

2. resuming lending to the economy;

3. developing the financial services market;

4. developing the capital markets’ infrastructure.

Maintaining the macroeconomic stability, in fact, means maintaining inflation at 5% +/- 1percentage points.

In addition, on page 16 it is stated that the achievement of the Strategy goals will be evidenced, in particular, by the following: “the central bank remains committed to a prudent monetary policy, inflation targeting and flexible exchange rate in the market.”

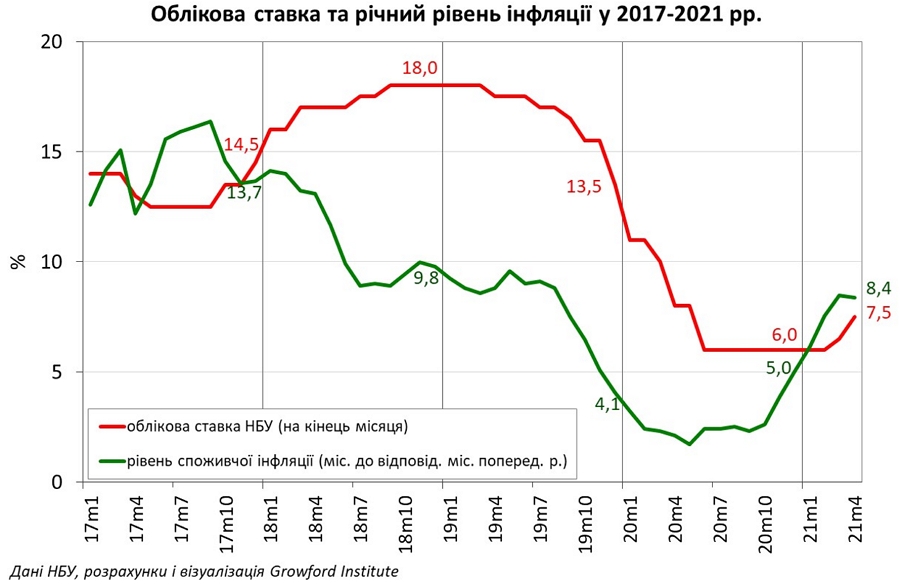

The Strategy does not refer to any easing of monetary conditions that could stimulate demand and help the economy recover. And the current monetary policy is very far from promoting economic growth.

This was especially seen in 2018-2019, when the excessively high key policy rate (which was several times higher than inflation) was one of the main reasons for the actual cessation of the credit process, declining business activity and plunging the economy into recession before the coronavirus crisis.The decline in industrial production and a sharp slowdown in real GDP was as far back as the IV quarter of 2019.

Source: National Bank of Ukraine, calculations and visualization of the Growford Institute

The easing of interest rate policy in 2020 (which ended in June) was insufficient, given the unprecedented nature of the crisis and the excessively tight “starting” monetary conditions.

Moreover, in March 2021, the National Bank of Ukraine began a new cycle of raising the key policy rate, completely ignoring the fact of further decline in production.

The first sentence of the “main part” of the Strategy on page 14 can also testify to the lack of changes in the NBU’s “philosophy”: “The NBU’s proper performance of its functions – delivering price stability and promoting financial stability – is essential for the development of the financial ecosystem and economic growth.”

That is, the National Bank of Ukraine sees only two functions for itself, interpreting the norms of the Law on the National Bank of Ukraine at its own discretion. The fact that in Article 6 entitled “Main Function” promoting sustainability of the economic growth and support the economic policy of the Cabinet of Ministers of Ukraine is third (after price and financial stability) does not mean that this goal / function can be ignored by the National Bank of Ukraine.

From this point of view, even the very “mission” of the NBU (page 13 of the Strategy) – ensuring price and financial stability with the goal of contributing to Ukraine’s sustainable economic development – is nothing but an arbitrary interpretation of the Law.

This could be left there, but for the strategic goal No. 2 “resuming lending to the economy.”

Since it is a rare case when the NBU recognizes, but does not deny its involvement in the credit process.

This goal was already announced in the previous version of the Strategy three years ago.

However, the results of this goal in 2018-2020 are more than modest: the volume of net loans to economic entities decreased by UAH 18 billion (4.1%) to UAH 432 billion.

The growth of total net loans of banks (by 7.1% to UAH 581 billion) was exclusively due to loans to individuals, the volume of which increased by UAH 57 billion (61.7%) to UAH 149 billion over three years.

In the report on the implementation of the previous Strategy for 2018-2020, the NBU explains the unsatisfactory state of implementation of this goal by the impact of the pandemic: “because of quarantine restrictions and market uncertainty, demand for all types of loans has decreased.”

In this case, it is not clear why the worst lending rates were recorded in 2019, before the pandemic.

The logic appears when one takes into account the extremely high level of the key policy rate and unreasonably strict requirements for assessing the amount of credit risk (NBU Board Resolution No. 351 of June 30, 2016), but the NBU categorically does not notice this.

The updated Strategy, unlike its predecessor, implies quantitative “indicators” of goal achievement.

Considering the goal of “resuming lending to the economy”, the main indicator is an increase in net bank loans (economic entities and individuals in general) from 13.9% of GDP at the end of 2020 to 22% of GDP at the end of 2024.

At first glance, it is quite a good goal, given that the corresponding ratio at the end of (not very successful) 2016 was 23.2% of GDP, and at the end of 2013 – 52.1%!

However, taking into account the NBU’s forecast for GDP growth and making the calculations, we find that to meet the above goal it is necessary that the volume of net loans during 2021-2024 should increase 2.5 times to UAH 1.4 trillion or 25 % annually.

Source: National Bank of Ukraine, calculations and visualization of the Growford Institute

But such pace of lending has not been observed in Ukraine since the 2008 global financial crisis.

And to achieve it without a significant easing of monetary policy and easing of standards for banks to build up reserves related to active operations (which the NBU is not going to do) is almost impossible.

It is much easier to stop the credit process than to “start” it again. One should not count on budget programs (such as “Affordable loans 5-7-9%” and “Affordable mortgage 7%”) in this matter – the budget will simply not be able to compensate for the growth rates of the loan portfolio by UAH 850 billion.

And taxpayers should not “pay” for the NBU failures.

The National Bank of Ukraine could easily contribute to the “development of the capital market infrastructure” (goal No. 4) and increase the volume of the secondary market of government issued bonds through its own operations with government bonds on the open market.

However, such measure will not be found in the Strategy. There are no logical explanations for this, there is only an unfounded unwillingness of the NBU to use such operations.

It does not make much sense to analyze the second “strategic pillar”. The NBU is simply obliged to respond to the challenges of the time and promote the development of payment infrastructure and its protection, regardless of whether it is “written” in the Strategy or not.

Otherwise, it will be replaced by the central bank of another country or the anonymous Satoshi Nakamoto.

Perhaps the only advantage of the updated Strategy is that it has quantitative indicators of the achievement of goals. At the very least, this will allow one to ask very specific questions to the NBU leadership at the beginning of 2025.

Unfortunately, the format of the strategy does not provide for responsibility for non-fulfillment of target indicators.

Without it (responsibility), all this “promotion of economic recovery and development” is just a PR stunt.

P.S. As early as June 17, we will see to what extent the next decision of the NBU Board on the key policy rate will correspond to the declared strategic pillar “promoting economic recovery and growth”.

Mykhailo Dzhus, Head of the Money Markets Department at the Growford Institute, for Censor.net.