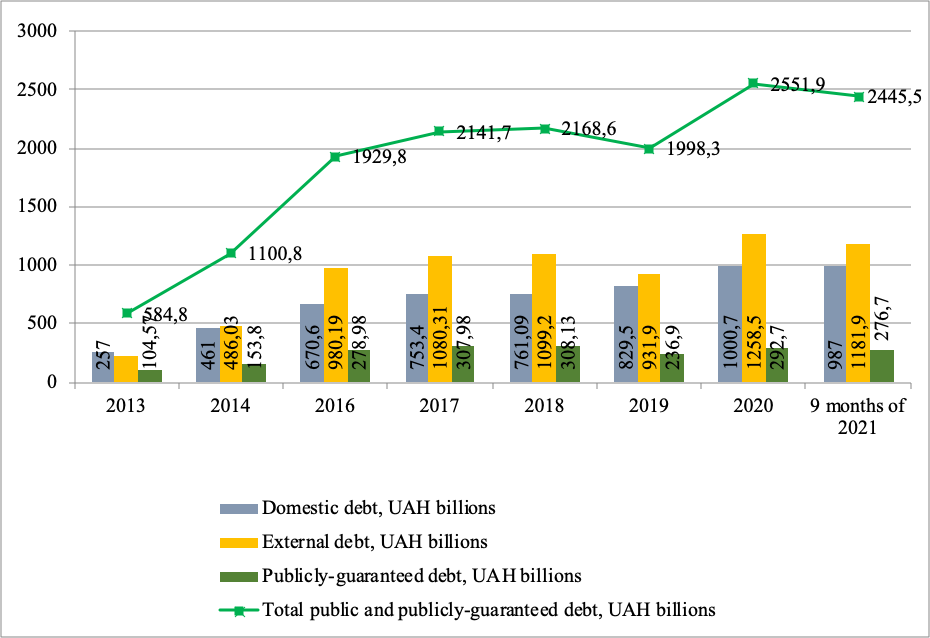

The dynamics of most debt indicators in 2021 was favorable compared to 2020. In January-September, the total public and publicly-guaranteed debt decreased by UAH 106.4 billion and reached UAH 2.45 trillion. Moreover, both domestic (by UAH 0.9 billion) and external public debt (by USD 0.5 billion) went down (see Figure 1). The level of debt risk also began to decline this year.

Source: Compiled by the author based on the Ministry of Finance of Ukraine data

Public and publicly-guaranteed debt relative to GDP in September 2021 was 50.8% of GDP, having significantly decreased since the end of 2020. The current relative level of debt is lower than the threshold of 60% of GDP. In terms of budget revenues, public debt in September 2021 amounted to 212.2%, having considerably improved compared to December 2020, when it was 237.2%. Thus, the dynamics of debt relative to budget revenues was downward, although the threshold was exceeded (200%).

The world’s accepted threshold of short-term external debt to international reserves is 100%.In Ukraine, it was 164.7%, which demonstrates the country’s poor international liquidity. However, the gradual decrease in the ratio of short-term debt to reserves reduces this problem.

Therefore, Ukraine violates two of the five key indicators of deb sustainability, which shows the preservation of certain solvency and liquidity risks for the public finance (see Figure 2).

Source: compiled by the author based on data from the IMF, the World Bank, the NBU and the Ministry of Finance of Ukraine

The government’s gross borrowing needs are also excessive. For instance, in 2021 it is estimated at 19.7% of GDP, which exceeds both the threshold (15%) and the average level in emerging market economies (13.6% of GDP). In the second half of the year, government attracted the EU macro-financial assistance, SDRs and IMF loans, thereby reducing the risk of debt refinancing. However, rising global interest rates will later raise the issue of the availability of debt refinancing sources.

The distorted structure of public debt by currency also poses risks to macro-financial stability. In September 2021, the share of debt denominated in hryvnia was only 37.1% of the total debt. According to another indicator, “the share of non-residents among the holders of general government debt”, the situation is also almost critical. In Ukraine, this share is 50.6%, and the average in emerging market economies is 16%. This indicates a high level of foreign exchange and refinancing risks in the structure of Ukraine’s public debt, which signals the possibility of debt complications in case of a sharp devaluation of the hryvnia or loss of access to external sources of financing.

However, even taking into account these risks, the amount of Ukraine’s public debt is insignificant in the international dimension. For example, the level of world public debt, according to IMF, at the end of 2021 will be 97.8% of GDP. In advanced economies, it is predicted to reach 121.6% of GDP, and in emerging market economies – 64.3% (see Figure 3).

Source: compiled by the author based on the IMF, Fiscal Monitor October 2021

In Ukraine, public debt is projected at only 54.4% of GDP. That is, among the emerging market economies, Ukrainian debt will lag behind the average by almost 10 percentage points of GDP.

Significantly, since the beginning of the epidemic and economic crises, the public debt has grown rapidly in many countries. According to the IMF, during 2020-2021 the average level of public debt in the world is to be increased by 14.2% of GDP. In advanced countries, public debt growth is projected at 17.8% of GDP. In Ukraine, the debt growth for 2020-2021 will be only 3.9% of GDP.

One reason for this is moderate fiscal policy. For instance, the consolidated budget deficit of Ukraine in 2020 was 5.4% of GDP, which is almost twice behind the world average – 10.2% of GDP. Ukraine’s consolidated budget surplus for the first nine months of 2021 is 0.1% of GDP.

These figures contrast sharply with the fact that in 2021 fiscal policy remains expansionary in the world: budget deficit in advanced countries is expected to decrease from 10.8% of GDP in 2020 to 8.8% in 2021, and in emerging market economies – from 9.6% of GDP to 6.6%.

In Ukraine, the cyclically-adjusted primary balance in the third quarter of 2021 reached + 3.4% of GDP (NBU estimates), while in the first and second quarters it was also positive. That is, fiscal policy has a depressing effect on aggregate demand.

Ukraine’s cyclically-adjusted primary balance is many times higher than the average in emerging market economies (-0.8% of GDP) and in emerging European countries (-1.8%). This shows that Ukraine’s fiscal policy is excessively tight in the international dimension. Figure 4 compares this indicator in Ukraine and in neighboring countries.

Source: Compiled by the author based on the IMF data, Fiscal Monitor, October 2021

The fiscal impulse in Ukraine in 2021 became negative, which meant a tightening of policy compared to 2020 and transition to the stage of fiscal consolidation. Significant tightening of fiscal policy in 2021 as the epidemic crisis persists and the economic recovery was weak was early and unjustified.

In the global context of the problem, a recent declaration by the leaders of the G20 at the Rome Summit states that the leaders of these countries remain determined to use all available tools for as long as required to address the adverse consequences of the pandemic, in particular on those most impacted, such as women, youth, and informal and low-skilled workers. The G-20 declaration also notes that the states will continue to sustain the recovery, avoiding any premature withdrawal of support measures, while preserving financial stability.

In most countries, fiscal policy continues to be expansive this year, and the fiscal rescue packages have already reached USD 16.9 trillion. Addressing the health emergency remains a global top priority for fiscal policy. Nevertheless, fiscal support for economy is still needed under quarantine restrictions and volatile economic recovery. In advanced economies, the focus of fiscal policy in 2021 is shifting from financing the emergency spending associated with the pandemic toward strengthening national economies through digital transformation, green transition and other long-term investments.

In many countries around the world, strengthening of fiscal frameworks to buttress policy confidence and limiting borrowing cost is needed. Fiscal frameworks comprise long-term fiscal targets, also called “anchors”; fiscal rules, which impose long-lasting constraints through numerical limits on fiscal aggregates; fiscal institutions and procedures that govern how budgets should be prepared, approved, and executed.

In all countries, strengthening fiscal frameworks can help buy time in an emergency and later begin to restore fiscal space. By achieving the confidence of creditors in the fiscal responsibility of the government and maintaining debt sustainability, the government gets the opportunity to finance the budget deficit and prolong public debt at reasonable rates. IMF experts rightly point out that commitment to fiscal discipline and clear communication of economic policy priorities, backed by fiscal transparency, can reduce borrowing cost.

In Ukraine, after overcoming the effects of the COVID-19 pandemic, from 2023 there will likely be an objective need to return to fiscal rules, in particular limits on budget deficit and debt ceiling. But the experience after global crisis of 2008 and the latest post–COVID-19 trends may provide an opportune time to redesign or recalibrate the rules. For Ukraine, it is suggested to slightly raise the debt limit to 70% of GDP, but with the expansion of its scope from the central government budget to the general government sector.

Another global challenge for Ukraine is the tightening of monetary conditions in the United States and other advanced countries in 2022, which will lead to growing global interest rates and the capital outflow from emerging markets. In order to mitigate the impact of these factors, vulnerable countries must create a “safety cushion” in the face of increased troubles in international markets (provide adequate size of international reserves), as well as reduce foreign currency debt.

Therefore, global financial risks should encourage the reorientation of the Government of Ukraine from external borrowings to those on the domestic markets and the using of the potential of the domestic financial market. In addition, an anomalous situation when the Government is willing to borrow in foreign markets at 6.3-8.5% in dollars while the rates on borrowings in the domestic market are twice lower, in particular, 3.8% for government issued bonds in dollars and 2.5% for government issued bonds in euros, should be stopped.

The effective coordination of fiscal and monetary policies and a moderate level of interest rates in the domestic capital market have been on the agenda in Ukraine for a long time. Increasing the participation of retail investors to invest into government issued bonds through forming appropriate organizational and financial mechanisms would strengthen the competitiveness of the market and would help reduce interest rates.

On the other hand, as noted above, taking into account the international experience and world leaders’ recommendations, in 2021-2022 Ukraine should avoid too active and too early withdrawal of fiscal support programs for the economy and social sphere, without ignoring the problem of macro-financial stability. This requires abandoning restrictive fiscal policies till the pandemic is overcome and economic activity is resumed, fulfilling existing plans to finance budget expenditures, and implementing tools to support business and the population during lockdowns.

Tetiana Bogdan, Doctor of Economics, Scientific Director of the Growford Institute for Dzerkalo Tyzhnia.